Hi guys,

Just drawing your attention to this cosmetics company that has been doing very well this year. It is not well covered, if at all, by sell-side analysts, yet is killing it on Taobao:

Rui Ma and Ying Lu‘s podcast are required listening, I also found this Motley Fool article helpful:

Hillhouse-Backed Yatsen Is Now Public. Here’s What Investors Should Know | The Motley Fool

This Chinese cosmetics company has positioned itself well for long-term growth.

https://www.fool.com/investing/2020/12/02/hillhouse-backed-cosmetics-company-yatsen-ipo/

Here are two questions I have:

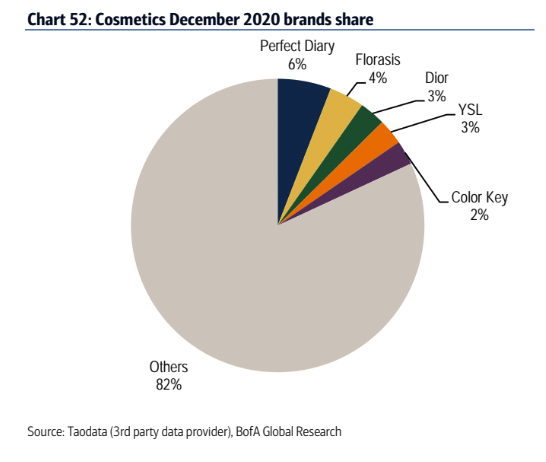

1. Is their market share meaningful? If you throw enough VC money or subsidise enough product (grow sales, but spend a lot of money on marketing), can’t anyone ‘buy’ market share, at least to start? 6% does not seem like a lot, and still far away from pricing power

2. Given it was only established in 2016, and doesn’t have much of a track record, do they have staying power, are they ‘built to last’? What happens to them when the other cosmetics houses start copying their tactics?

What issues jump out at you, when thinking of this one?

COMMENTS

-

Yes their marketshare is meaningful in that they were able to carve out the path to become the domestic market leader when other domestic brands or even international brands have the same access to capital. In terms of pricing power that’s not that they’re after anyways. Their entire product strategy is 大牌平替 aka becoming the direct substitute for the big brand products at economical prices. They can maintain their gross margin because while they charge much less for their products, they also spend a lot less on marketing.

As for staying power, just today I was listening in on a clubhouse room talking about how luxury beauty brands (Dior, Armani, Lancôme etc) have approached the Chinese market and because of how fast the Chinese market took over Japan to become the worlds second largest cosmetics market many of these brands are still trying to find the right strategy in China and capital commitment to marketing etc is still being experimented on. This shows global marketing spent for these brands are still way larger than what they’re spending in China right now. So from the looks of it right now domestic brands owns an operational advantage in the Chinese market but Eventually more and more resources will be poured in to fight in this market and domestic brands don’t really have strong moats to protect their marketshare other than pricing advantage. It will be a brutal war and there’s no guarantee who will survive which is also probably why they pushed to ipo so quickly lol. Strike the iron while it’s hot and cut the chives.

-

@Michael Hsieh To add to Michael’s comment, beyond the price element, take a look at their brand story in China, which is mentioned nearly every time they get press:

“哈佛大学的品牌创始人和英国时尚设计师在伦敦相遇,希望有机会把欧美彩妆风尚带回亚洲,在视觉形象上有所突破。”

“The Harvard brand founder and the British fashion designer met in London and wanted the opportunity to bring the European and American makeup trends back to Asia with a breakthrough in visual imagery.”So yes, they can go acquire some other “more Chinese” brands, but I just don’t think that is how this team sees the world. Given they started in 2016 when the world was a bit simpler and not as much “East vs. West,” it makes a lot of sense.

-

I met the CEO a couple of years ago in New York. The entire strategy started with colour cosmetics which is easier for companies to push through e-commerce and convince people to ‘try’. I believe they recently started with skin care which has historically been a harder game, especially on the higher end where international brands (Estee/Amorepacific etc) has historically been more successful.

-

@TheMadman I think they’ve made some acquisitions to help bolster their push into skincare. But yea its definitely a much much more competitive market but they kind of have to fight that war if they really want to be the L’Oreal of China lol.

-

@Michael Hsieh agree pricing power is not something that is important for them right now

but L’Oreal isn’t used to playing the honest prices, quality goods 价廉物美 game, is it? when I think of these European/Japanese brands, it is all about exclusivity and charging high prices… are you saying the luxury brands are willing to dirty themselves, and burn cash to compete in the lower price brackets?

I think the Koreans started doing that first, with Innisfree, etc? but then they got shut out because of THAAD, and maybe these guys are trying to fill the gap they left, and use their business model + Chinese social media characteristics

from the videos I’ve seen so far the vibe I am getting is, affordable and fun: this one is a good example. how much more internet meme friendly can you get, to have a cat themed beauty box 🐱

@TheMadman what did you think of the CEO? senior management have all crossed through the same uni, when reading their bios I couldn’t help but think of the movie American Dreams in China (中国合伙人) which is roughly based on the founders of New Oriental – can imagine them being mates and working closely together, but if there is a falling out…

-

L’Oréal also have many brands in their portfolio that is targeted towards the lower end of the market so it really just depends how aggressively they want to pursue that part of the market but I was speaking more about how the big brands L’oreal, Estée Lauder etc will invest more and more into building the necessary “infrastructure” to do everything that domestic players can do digitally as well as getting right endorsers/KOL for their products.

Also funny you mention that movie, cause one of the founders of new oriental, Xu xiaoping, who is also the founder of zhenfund, was the biggest early backer of Yatsen and Xu met with the founder before he started Yatsun

-

@Michael Hsieh i think they will have to do this eventually but dunno if they can get it right straightaway – despite already having the lower end products and the brand presence, they lost the lead, right?

talking about this with you guys makes me more negative about the traditional players, not nec more positive about Yatsen 😜

i wonder to what extent the shareholders of the trad players will let them spend money in a market where there will be no return for years (brutal competition). if there is any weakness in their own home market, they will cut back. even if they ‘win’ the average ticket size would be so small relative to what they are used to, and make little difference to overall p&l. the temptation to just play it safe and avoid China or stick to what they already know seems quite strong

@Rui Ma tying this in to your points about culture, I agree. funny thing is i expect the CEO to agree too, it is just that they have to build the market first?

what i mean by build the market is, with 600mn people on $140/month, there is likely a lot of people who don’t use makeup, so this could be entry level for them? I think they will go for the $20 Paris-themed box and skip the trip to Paris rather than the $40 延禧攻略 one. a few years later, once they have traveled a bit and realise Paris smells rather different than it looks, this is when they consider the premium local offering

building the market also opens up space for its competitors, as it grows the market for them, rather than make Yatsen fight for it – win/win

I loved the Florasis concept, it totally is coming from the right place, but i wonder if it is over-engineered, and more costly (production cost) then necessary, some of that stuff is really OTT (example), and the market is confined to China. if i was the Yatsen CEO i would sell a bigger TAM as it includes the international market, which will raise more money, and then if a local brand slips up, say its costs go out of control, do an acquisition, and solve it 😝

-

@QuanNM It was a pretty short meeting and a lot of it was related to recruiting of MBA students so I didn’t get a strong feel about the CEO himself. That being said my point would be that the ultra premium products (think La Mer’s and La Prairie’s of the world) will be difficult to replicate.

-

So most of my comments are in the podcast episode but this is the main thing I want to highlight:

Perfect Diary is riding the DTC new, more-localized-and-thus-nimble brand wave but not the Chinese culture wave. That is, they are using supply chain knowhow and data-driven marketing and the ability to fully exploit China’s new influencer / social marketing platforms (foreign firms will be slower to react) but they are doing so using a Western theme. Take a look at all of their brands / marketing, and even their brand story of “we studied abroad and felt that we could do these Western products better.” Florasis (which BigOne Labs data show to be surging, and which anecdotally feels true), on the other hand, is doing both. The Chinese culture wave is huge and should not be underestimated. People in China my age (born 1981) will likely be less affected by it, but Gen Z is very different. From a macro perspective, I was very swayed by Li Lu’s argument in his essays that China will eventually default to its own culture because it is the most comfortable, and because it is fully integrated into society whereas foreign culture will always be awkward and have to be accommodated. Beauty is especially cultural. I am not even that “Chinese” culturally myself and Florasis simply the name already evokes a certain type of beauty for me that is entirely consistent with the visual and literary style of mainland China, historically and today. (If you read Chinese, even the translations of Estee Lauder and Lancome are very consistent with Chinese conceptions of beauty, which is very much flower & nature based.) With cosmetics conglomerates, this can be easily amended with acquisitions and new brand launches, but so far Yatsen seems totally wedded to a foreign conception. That’s not to say that they don’t have Chinese elements in their products, but that it’s very muted, and in fact is the reason I believe they must compete on price. Florasis is 2x their price. Again, I’m not saying that Florasis is going to win, I’m just saying that I’d be more inclined to bet on someone who exploits all the advantages, including culture.

-

@Rui Ma I saw this interesting clip about Florasis that was cut from some interview. Austin Li has also been pushing for this cultural transformation for domestic brands. http://xhslink.com/xyVOkb

-

@Michael Hsieh Summarizing for those who do not read Chinese here. Florasis went to Austin Li (#2 livestreamer in China pretty consistently over the last 3 years, known for cosmetics and lipsticks in particular), a few years back and gave him a crap product. He told them it was terrible, and they invited him to help co-create a product that would “wow” him (one of his well-known phrases, haha). And after two years, they came up with this series of products based on Chinese carvings.

The point is to do something “big brands” ie the Western brands cannot think of to do. To do something totally different. (So it is still about innovation in product design.) And if you think about it, that thing is Chinese culture. My two cents.

Addendum: I do not think this is by any means some kind of proprietary IP — you can go on Taobao and see cheaper knockoffs for both Florasis carved series and anything Perfect Diary does. It’s more about the branding itself. A great example is the concept of luxury in cosmetics. With Perfect Diary, one of their collaborations is with the Met, which featured paintings of European royalty and the like. With domestic Chinese brands such as Florasis, they feature the Forbidden City. You could argue that the Met is harder to get and that in fact shows Perfect Diary’s strengths in BD (business development), but it’s the Forbidden Palace that will crank out hit IP after hit IP (I’m talking about Chinese mini series featuring ancient China). All that being said — Perfect Diary isn’t stupid, they also have a good amount of anime-based IP palettes and such, which are Asian and very popular, but not particularly Chinese. However, it is important to note that foreign content has never really accounted for more than 10% of total traffic on any of the mainstream long video sites (I’m excluding Bilibili here) — not even the massive Korean hits.

-

Somewhat off topic but any thoughts on whether traditional departmental stores like Parkson Cosmetics have any chance of transforming and competing in this new age of cosmetics selling and marketing?

-

@Khang Wei Koo Depends how aggressively they’re willing to push their private label brands, and if they can find a platform partner to provide the offline end of some sort of online+offline experience. In China it would be very hard for them to have enough leverage power to obtain exclusive skus or online marketing promotion with the big brands, so it would have to be their own private label brands or a collection of small brands that are willing to work with them in exchange for increase exposure.

-

@Khang Wei Koo places like Watsons have been very successful with their white labels / owned labels in skin care, you can see the effect in the consolidated margins of the business (much higher than typical pure distribution). Part of how they have done is by leveraging their existing interactions with customers, I was given this example by a person at the company: through their membership program, they send a RMB20 coupon, to redeem it you need to pick ahead the product category where you are planning to spend it, this gives info to the company on expected demand next month by region for say “anti shine face cream for oily skin”, Watsons proceeds to load that store section with 2 or 3 of their owned labels in that product alongside 2 main brands. The cannot create trend, but they are pretty efficient to capture the dollars out of it.

-

@Khang Wei Koo I wanted to share about this new brand I just heard about today on 疯投圈 (Chinese podcast), Harmay on their episode 51. It’s a new type of offline store, trying to be China’s Sephora, I guess, except with a higher end look and feel (and arguably, in brand selection that I can see). I don’t know that they do their merchandising any differently, but am impressed by how different their aesthetic is. I do think the next stage of Chinese offline retail will look very different, so Parkson and the like should watch out, regardless 😆

-

hi guys, Gong Xi Fa Cai, 新年快乐!

just a recap here, also threw in a few things I learnt:

1) pricing power is not important right now, focus is on market share. it seems there has been some history of finally arriving there after trial and error, and in more recent history some consistency in maintaining that position as well, it isn’t entirely ‘bought’, also recognising if they did engage too blatantly in this, others could well do it too

2) there’s a real risk the established houses might start (ok, will start) copying the social media tactics that PD has used successfully so far, and this will test their (weak) barriers to entry when they do. not going to be easy, though will note that for the trad players they might be structurally disadvantaged because they don’t have the same p&l on China

3) how can you expect Yatsen to be truly dominant abroad if it is not first dominant at home, and how can you expect it to be dominant at home if it doesn’t have a brand that addresses local culture? so PD is a brand under the group, this means at some point (who knows when) to meaningfully get to a L’Oreal you can expect a different brand that addresses local culture. this is great for TAM and revenue expectations, to the extent there are even expectations as there is still barely any coverage

4) long term credibility also requires them to have some degree of vertical integration (R&D, own manufacturing facilities, etc) and this will be really expensive and time consuming, but frankly they have to do it, so if they spend too much time further down the value chain, whilst neglecting this buildout, this is a negative

5) the role of the ODMs (the contract manufacturers, such as Cosmax), they seem to be the ones that are getting the most out of this arrangement. PD’s emphasis on volume means the ODMs will see their capacity taken up, this will get squeezed even further should the trad players take the gloves off

6) ultra premium – forget about it. maybe in 10 years?

7) some doubt as to whether they can be as successful in skin care

8) traditional retailers advantage is to cross-sell their products at low cost, which is accretive to their margins. they will have to watch out for the online players that start pushing in to their territory though

9) (new to me) is a Chinese tech VC podcast, Crazy Capital 疯投圈, which is going to be hours of good listening, will be good to have a series to compare to the GGV Capital one

overall I feel more comfortable about their prospects in the short term, they have some momentum going for them and it is pretty believable they can use the IPO money to just keep doing more of the same, which will work for them – for now

however the further out one looks, the harder it is to gauge if this one is a keeper, especially with the wars to come. that will need a different level of due d, one to watch for sure

stay safe guys, happy weekend and 牛 year to all

-

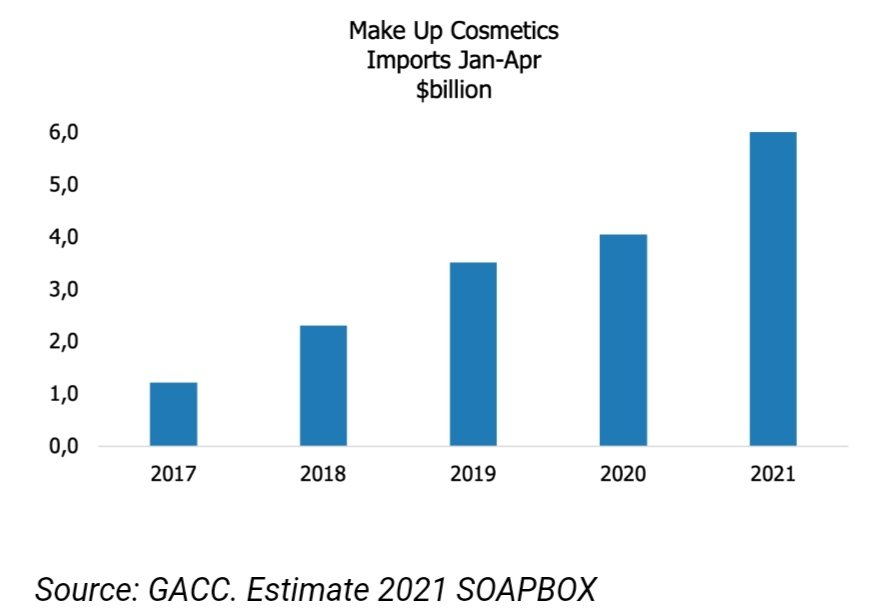

found this useful piece of information from Soapbox, one of the free mailing lists I subscribe to, about the Beauty category being quite a big deal for Chinese imports

Here’s a brief extract:

We reveal the top 5 categories in the first four months [of 2021].-

Frozen meat $6.5 billion

-

Beauty $6 billion

-

Cars (4WD, SEDAN less than 2000 cc) $6 billion

-

Medicaments $4.9 billion

-

Diamonds $3.1 billion

-

They argue that Beauty is inevitably the top FMCG import category, as cars and diamonds don’t count as fast moving, and meat is a consumer staple.

So related to Yatsen’s positioning as a ‘Western-brand’ substitute, makes for an interesting, dual circulation aligned, approach that maybe gives it a different spin as to why they have not introduced local brands that prioritise Chinese culture and Chinese characteristics.

The rest of the mailing is also worth checking out, as it picks up a bunch of other interesting things, another being where the Chinese government gets its tax revenue from (mostly VAT and corporate taxes). I’m not affiliated with them, signed up awhile ago, then forgot about it, & luckily opened it & happened to read.

More here: https://mailchi.mp/0b833b9cdf6f/6bdeg423g1

it was reported in July that one of the co-founders, the COO, 陈宇文 Vincent Chen resigned in July for ‘health and other personal reasons’

last month, in the Q2 earnings call, in August, the CEO clarified that he left ‘because of the health issue, and actually left around April’

in my experience, health is not usually a good reason to leave, at least abruptly. I am thinking of the old school manager type that will carry on working to pass on duties and responsibilities (a year?), and not ‘be a consultant’

certainly, this is no longer the management team we thought we were getting

what do you guys think happened?

-

@QuanNM Missed that! I think overall there is (and was, from the get go actually) a lot of skepticism that they can acquire and retain customers profitably. There were a lot of funds poured into DTC brands overall in China YTD especially, and I’m not sure if makeup was a top category (seemed to me food in general was) but it’s up there.